A new survey shows that more than three out of four people who consume THC-infused cannabis beverages drink less alcohol—with more than a fifth saying they have quit alcohol entirely.

The poll, published on Tuesday, was conducted by THC beverage company Crescent Canna, which surveyed its customers about their use of THC drinks.

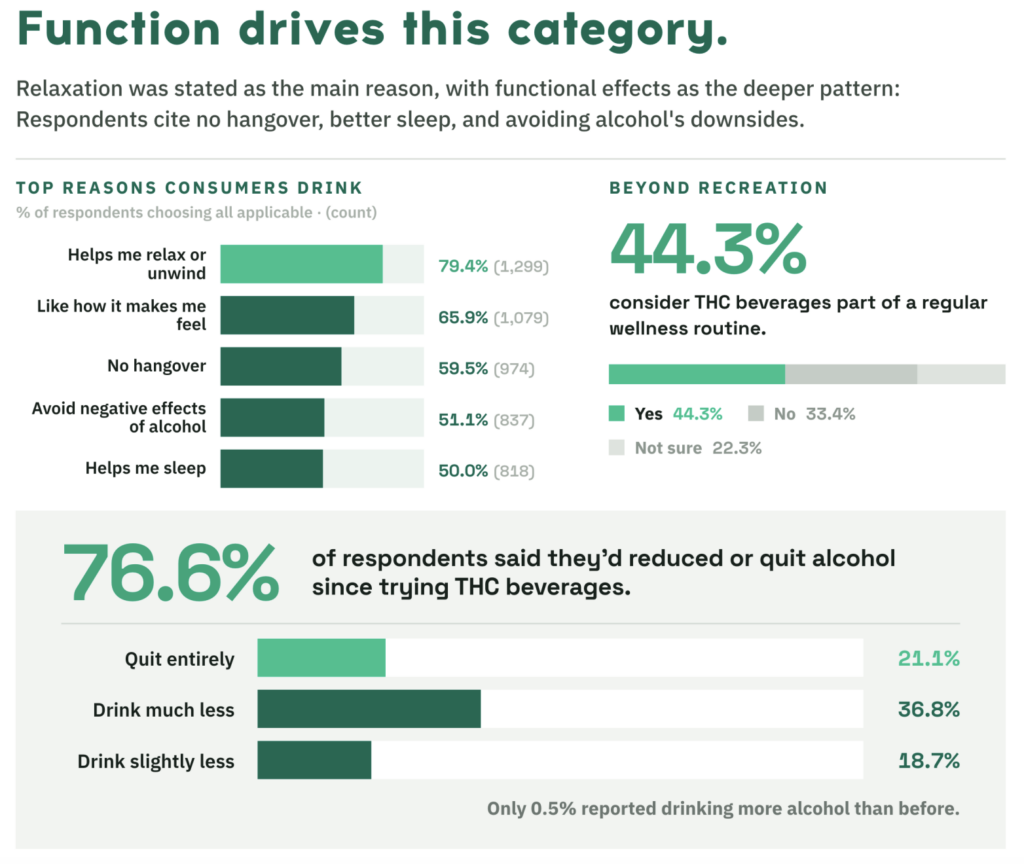

Since first trying the products, 37 percent said they drink much less alcohol, 19 percent drink slightly less and 21 percent have quit alcohol altogether.

Forty-four percent said that THC beverages have become part of their regular wellness routine.

When asked more specifically why they like cannabis drinks, 80 percent said the products help them relax or unwind and 50 percent said they use them as a sleep aid.

More than half (51 percent) said THC beverages help them to avoid the negative effect of alcohol, and 60 percent said there is no hangover.

Via Crescent Canna.

More than a third of THC drink consumers (35 percent) said they end up using other cannabis products less often due to the availability of the beverages. Another 15 percent said they exclusively consume cannabis in drink form.

Consumers, meanwhile, are broadly aware of the looming federal recriminalization of hemp-derived THC products that is set to take effect in November, with 87 percent saying they know about the planned ban.

Twenty-seven percent said they are either actively stocking up on THC drinks or buying them more often in preparation for the federal crackdown, and another 41 percent said they plan to as November approaches.

If the ban goes into effect as scheduled, 67 percent of THC drink consumers said they would turn to other forms of cannabis and 23 percent would start drinking more alcohol. Just 8 percent say they would stop using THC entirely.

For now, the vast majority of consumers (63 percent) say they are buying cannabis drinks online, while another 26 percent say they obtain them at grocery, liquor, convenience or specialty retail stores. Five percent get THC drinks at marijuana dispensaries and another 5 percent buy them at bars, restaurants or event venues.

The poll involved interviews between May 29 and June 11 with 1,637 adults over the age of 21 who have tried a THC beverage at least once.

An earlier poll conducted by Crescent Canna last year similarly showed that nearly four in five adults who drink cannabis-infused beverages say they’ve reduced their alcohol intake—and more than a fifth have quit drinking alcohol altogether.

A separate recent survey from cannabis telehealth platform NuggMD found that marijuana consumers shows they are overwhelmingly more likely to want to dine at restaurants that offer cannabis-derived THC drinks as an alternative to alcohol.

A previous NuggMD poll found that cannabis consumers are more likely to shop at Target following the major retailer’s decision to start selling hemp-derived THC drinks,

The latest poll results on consumer preferences come as lawmakers from both major parties have filed various pieces of legislation to delay, alter or reverse the impending federal recriminalization of hemp THC products and as the White House pushes Congress to act on the issue.

Hemp derivatives with less than 0.3 percent delta-9 THC on a dry-weight basis were federally legalized under the 2018 Farm Bill that President Donald Trump signed during his first term in office. But late last year, he signed new legislation containing provisions that will redefine hemp to make it so only products with 0.4 milligrams of total THC per container will remain legal after November 12.

In a letter to House Speaker Mike Johnson (R-LA) last month, White House Office of Management and Budget (OMB) Director Russell Vought said the administration wants lawmakers to “ensure the fair treatment of hemp products”—specifically citing legislation that would keep many hemp products legal that are currently set to be recriminalized this year, add labeling requirements and institute new taxes on sales, among other regulatory reforms.

The administration “welcomes the opportunity to work with the Congress to, at a minimum, update the statutory definition of final hemp-derived cannabinoid products to allow Americans to benefit from access to appropriate full-spectrum CBD products,” OMB separately said last month, “while preserving the Congress’s intent to restrict the sale of products that pose serious health risks.”

The call to avert a broad prohibition on hemp CBD products was included in a statement of administration policy about an annual agriculture spending bill that passed the House of Representatives.

Several lawmakers had filed amendments to that legislation to keep hemp products legal, but each was either blocked by the House Rules Committee from advancing to a floor vote or withdrawn by its sponsor.

“The Administration supports advancement of this legislation, but looks forward to addressing its concerns prior to enactment,” OMB said in its statement of administration policy. “The Administration looks forward to working with the Congress to provide more input as the bill’s legislative process unfolds.”

In April, the president himself urged congressional lawmakers to again redefine hemp to avoid recriminalization of full-spectrum CBD products.

“I am calling on Congress to update the Law to ensure that Americans can continue to access the full-spectrum CBD products they have come to rely on, and that help them, while preserving Congress’s intent to restrict the sale of products that pose Health risks,” Trump said in a Truth Social post on the same day his administration announced it is moving forward with rescheduling marijuana.

“We must get this done RIGHT and FAST, especially for those who saw that CBD helps them,” he said. “Plus, I am told it will also help our GREAT FARMERS, who we love, and will always be there for.”

Industry advocates say that the law as enacted last year not only threatens to prohibit intoxicating and synthetic cannabinoid products but also stands to remove popular full-spectrum CBD products that many Americans use therapeutically from the market.

“ONE in FIVE adults used it in the past year, and many say it improved their chronic pain enormously,” the president said in his social media post, adding that hemp-derived CBD “has made a HUGE difference for so many people.”

He also referenced a new initiative the administration launched in April to cover up to $500 worth of hemp-derived products each year for eligible Medicare patients. The program being implemented by the Centers for Medicare & Medicaid Services (CMS) focuses largely on CBD but also allows products to have up to 3 milligrams of total THC per serving.

“In December, I signed a very important Executive Order calling for Research and Innovation for Hemp-derived CBD,” Trump said. “Our wonderful Dr. Mehmet Oz moved fast to follow the directive in the Executive Order, and launched a model for some Seniors earlier this month. But more must be done!”

“Please get it done, and SOON,” the president said in reference to a congressional fix for the broad recriminalization set to take effect in November. “Thank you for your attention to this matter!”

It’s not clear how far Trump wants to scale back the scope of the scheduled federal restrictions on hemp products and what kinds of revised THC rules and limitations he would prefer to sign into law.

As Marijuana Moment reported last month, a Republican congresswoman is circulating draft legislation that would keep hemp THC beverages legal under federal law, creating a carve-out from the broad recriminalization of products derived from the crop that is set to take effect later this year.

The Hemp-Derived Beverage Regulatory Clarity Act from Rep. Beth Van Duyne (R-TX), in its current form, would allow adults over 21 to purchase and consume hemp THC drinks with up to 5 milligrams of delta-9 THC per serving. It would also impose a federal tax of 10 cents per milligram of any hemp-derived cannabinoid contained within such beverages.

The National Restaurant Association, which represents the industry, recently sent a letter urging congressional leaders to delay the federal recriminalization of hemp THC beverages that is scheduled to take effect later this year and replace it with a regulatory framework that “ensures consumer safety while meeting growing market demand” for the products as an alternative to alcohol.

A U.S. Department of Agriculture report published in April shows that farmers in the U.S. grew three-quarters of a billion dollars worth of hemp crops in 2025—a 64 percent increase from the prior year.

Marijuana Moment is made possible with support from readers. If you rely on our cannabis advocacy journalism to stay informed, please consider a monthly Patreon pledge.